investing

-

Many clients are surprised when banks offer lower borrowing capacities than expected. This is due to the bank’s use of buffers, benchmarks, and assumptions that impact perceived income. Factors include interest rate assessments, the Household Expenditure Measure, and the treatment of existing debts. Understanding lender policies and improving financial statements can help maximize borrowing potential.

-

Reverse mortgages explained in 2026: who they suit, who they don’t, how the Home Equity Access Scheme compares, and the questions to take to your accountant and solicitor.

-

Lenders Mortgage Insurance (LMI) protects lenders if borrowers default when their loan exceeds 80% of a property’s value. While often avoided by saving for a 20% deposit, waiting can lead to missed property value growth. Alternatives like government schemes and guarantor loans exist. Informed decision-making is crucial based on individual circumstances.

-

Interest-only loans can provide lower monthly payments and potential tax benefits for property investors but come with risks like rising repayments after the interest-only period ends and lack of equity building. They suit those with clear financial strategies, particularly investors, rather than owner-occupiers without a plan. Understanding these loans is crucial before committing.

-

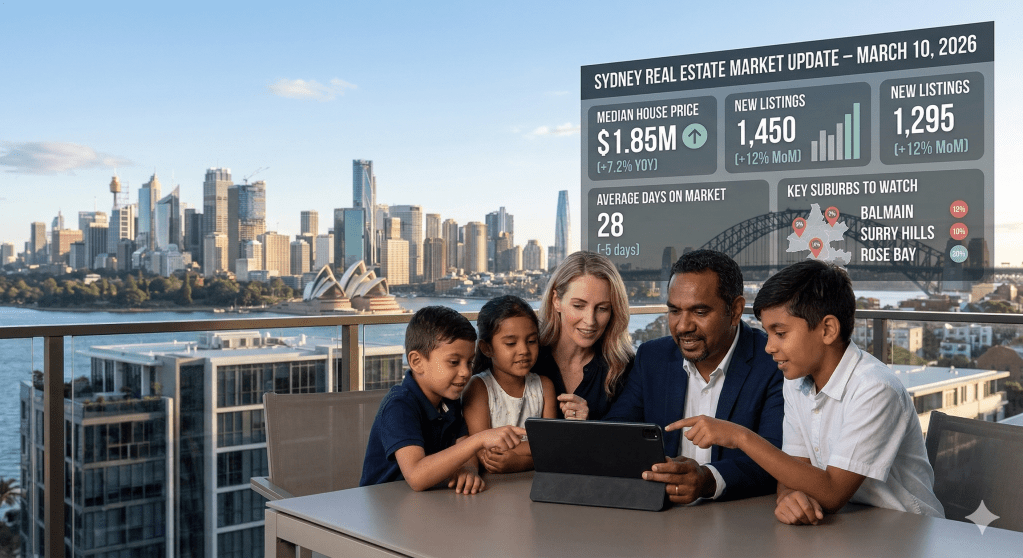

As of March 2026, Sydney’s property market shows renewed buyer confidence due to steady interest rates and expanded government deposit schemes, attracting first-time buyers and investors. Increased competition exists, yet buyers approach with caution. To navigate this dynamic landscape, it’s essential to secure pre-approval, focus on personal needs, and seek expert guidance.

-

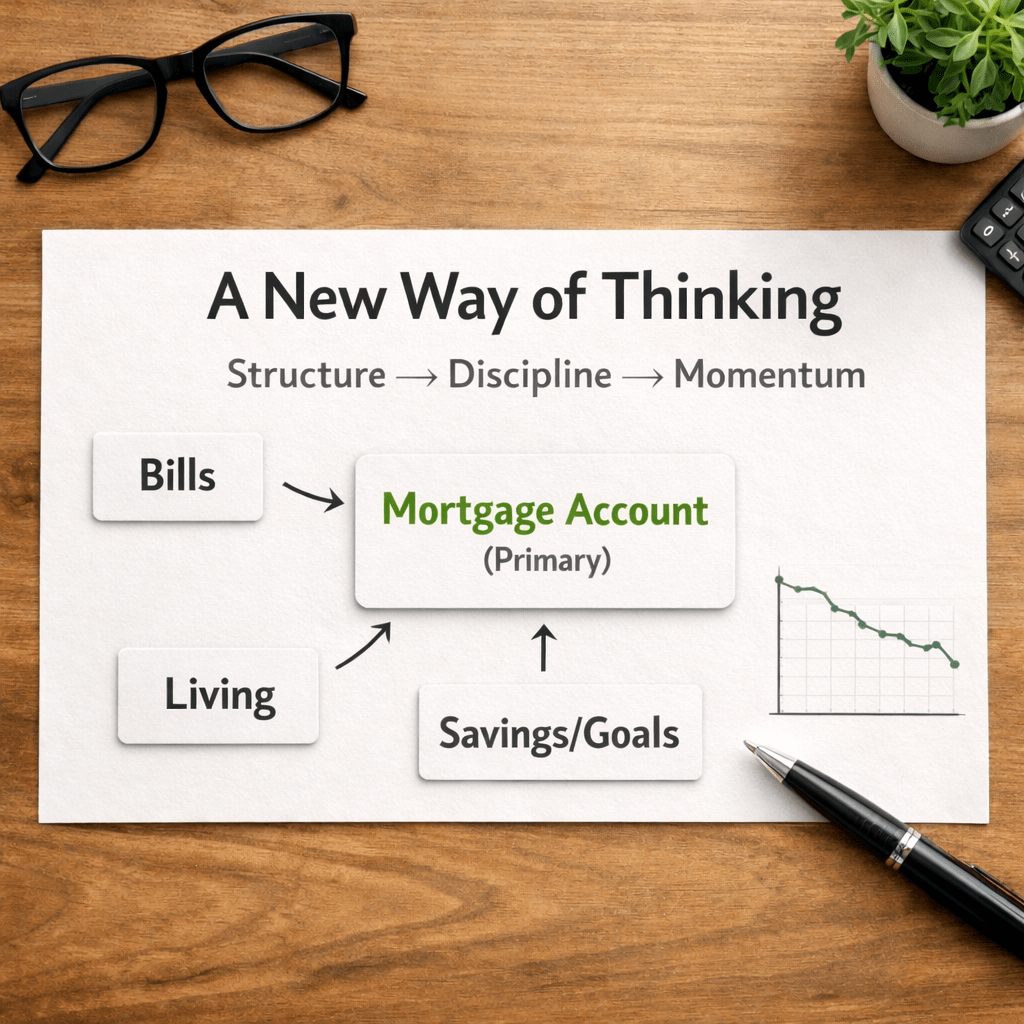

The article emphasizes the importance of loan structure over merely chasing lower interest rates in mortgage management. By restructuring income streams through a mortgage account, borrowers can create discipline and momentum in debt repayment. This approach enhances financial awareness and can lead to significant long-term savings and reduced loan terms.

-

The Home Guarantee Scheme (HGS) helps Australians buy homes with lower deposits, sometimes as low as 2%, by eliminating Lenders Mortgage Insurance. It includes options for first home buyers, regional buyers, and single parents. Eligibility varies, but the scheme aims to make homeownership more accessible and encourages regional development.

-

I’ll be upfront with you, when I’m buying property for myself, I use a buyers agent. Every single time. And when my clients are out there hunting for their next home or investment property, I recommend they do the same. You might be wondering why a mortgage broker would push buyers agents so hard. After…

-

I get asked this question almost daily: “Should I refinance home loan now, or wait?” The honest answer? It depends entirely on YOUR situation. What I can tell you is that 2026 has created some interesting conditions, and if you’ve been sitting on the fence, certain signs might be flashing bright green telling you it’s…

-

Your home loan might be costing you thousands more than it should. And the harsh reality? Most Australian property owners don’t realise it until years down the track. With over 30 years of experience helping clients navigate the mortgage landscape, I’ve seen countless homeowners and investors paying far more than necessary, simply because they set…