As a mortgage and finance specialist, I spend a lot of time reviewing rates, comparing lenders, restructuring debt and negotiating sharper terms for my clients.

But after years in this industry, I can tell you something with certainty:

Loan structure and behaviour will outperform rate chasing every time.

Yes, interest rates matter.

Yes, product features matter.

But the way your cash flows through your life — and how disciplined that structure forces you to be — is what determines whether you’re still paying off your home in 30 years… or significantly sooner.

This blog is about a different way of structuring your mortgage — one that can create real momentum and provide what I call a Newstart to finance.

⸻

The Traditional Model (And Why It Drifts)

Most households operate like this:

1. Income goes into a transaction or savings account.

2. Bills and lifestyle spending come out during the month.

3. The mortgage repayment is deducted on its due date.

4. Whatever is left over is either saved or absorbed into lifestyle.

This system feels normal. It’s how most banks set things up by default.

The problem?

There is no structural pressure to prioritise debt reduction.

There is no friction to slow discretionary spending.

There is no built-in momentum.

Spending expands to fill available space.

And if surplus cash sits in a standard account, it rarely stays untouched.

⸻

Where Offset Accounts Fit In

Offset accounts are an excellent tool. I recommend them frequently when they align with a client’s situation.

An offset reduces interest by lowering the effective loan balance while keeping funds liquid. It provides flexibility, liquidity and tax planning advantages (particularly for those thinking long term about investment strategy).

But here’s the reality:

An offset improves the mathematics.

It does not enforce behaviour.

If $40,000 sits in an offset but is constantly dipped into for lifestyle upgrades, holidays or impulse purchases, the long-term acceleration effect weakens.

Offsets work best when discipline already exists.

Not everyone thrives in that environment.

⸻

The Alternative: Making the Loan Your Primary Account

Now let’s talk about the alternative structure.

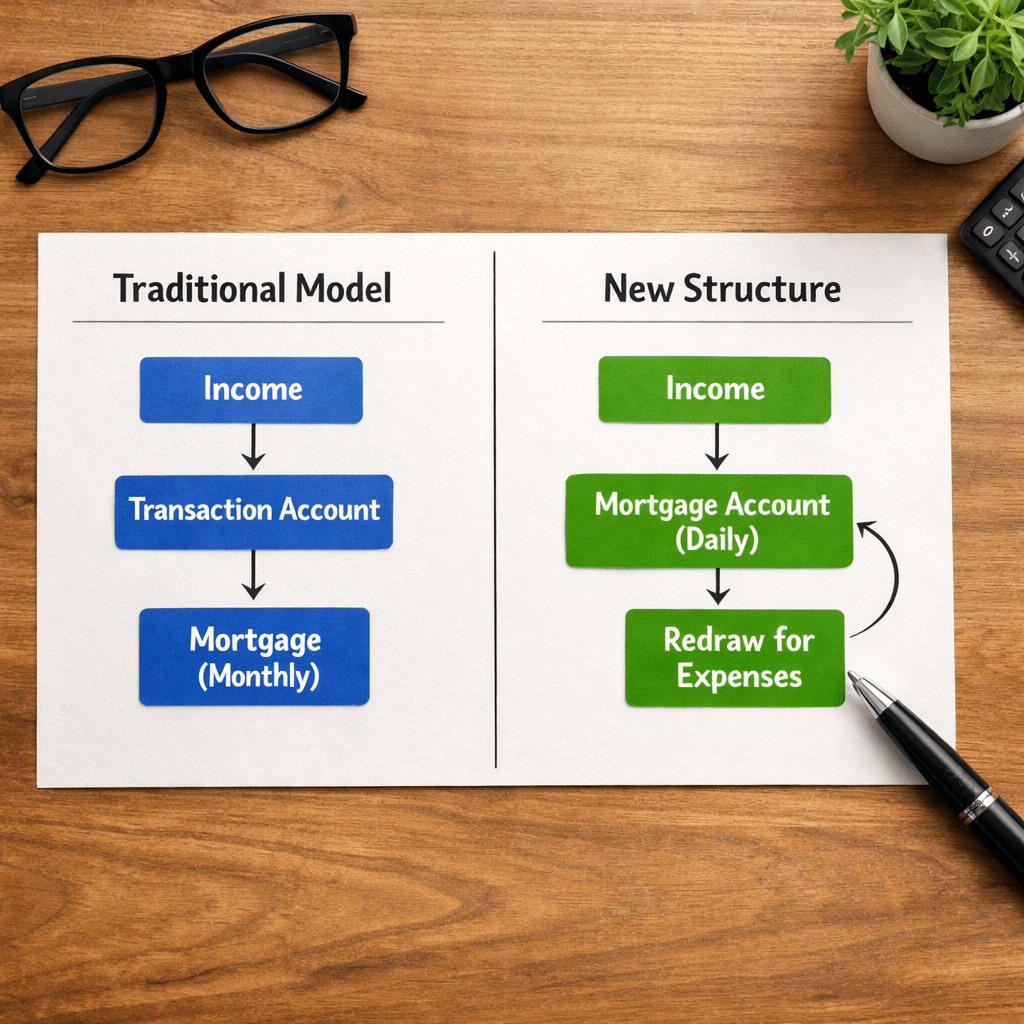

Instead of:

Income → Transaction Account → Mortgage Repayment

We restructure it as:

Income → Mortgage Loan Account (or fully transactional loan with redraw)

Every dollar earned immediately reduces the loan balance.

You then draw out only what is required for bills and living expenses.

This shifts the psychology entirely.

Your mortgage stops being a monthly bill.

It becomes your central financial hub.

⸻

Why This Structure Creates Discipline

This is where the strategy becomes powerful.

When surplus funds sit in a transaction or offset account, they feel like savings.

When surplus funds reduce your mortgage balance, they feel like progress.

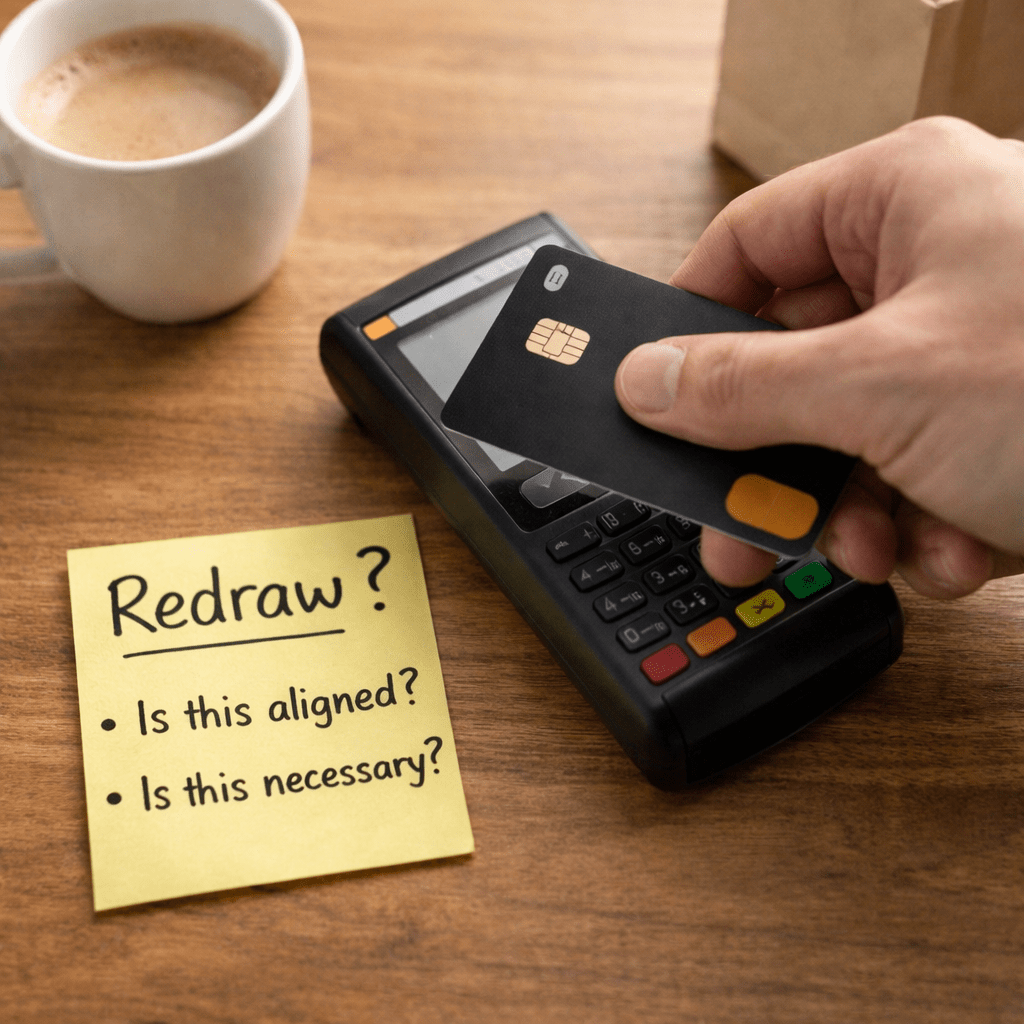

To spend money under this structure, you must consciously redraw it from the loan. That extra step introduces friction.

And friction creates decision-making.

Instead of casually tapping a card, you ask:

• Is this necessary?

• Is this aligned with our goals?

• Do we want to slow down our loan reduction for this purchase?

That pause is often the difference between financial drift and financial momentum.

The structure does not rely purely on willpower.

It embeds discipline into the system.

⸻

Example 1: The $700,000 Mortgage

Let’s walk through a practical scenario.

Loan: $700,000

Rate: 6%

Standard repayment (30 years): approximately $4,200 per month

Under a traditional structure:

• Income goes into a transaction account.

• Mortgage is paid once per month.

• Average daily balance remains close to $700,000 for most of the month.

Now, restructure it:

• Household income of $10,000 per month is deposited directly into the loan.

• Throughout the month, $6,000 is drawn out for living expenses.

• The loan balance drops immediately when income arrives.

Even though the net surplus hasn’t changed, the average daily balance is lower across the entire month, which reduces interest charged daily.

Over time, this compounds.

More repayment goes toward principal.

Principal reduces faster.

Interest shrinks faster.

That’s how acceleration begins — without increasing income.

⸻

Example 2: The Behavioural Shift

Client scenario:

Household earns $180,000 per year combined.

Good income. Stable careers.

But after reviewing spending, we identified:

• $1,200 per month in discretionary “leakage.”

• Subscriptions.

• Dining out creep.

• Unplanned purchases.

Under the traditional structure, that money was simply absorbed into lifestyle.

Once income began flowing directly into the loan, every discretionary purchase required a redraw.

Psychologically, this changed everything.

Within three months:

• Discretionary leakage reduced by $800 per month.

• That $800 went directly toward principal.

• The loan term reduced by years — not months.

Same income.

Different structure.

Different behaviour.

⸻

The Mathematics Behind Daily Interest

Mortgage interest is calculated daily, not monthly.

If your loan sits at $700,000 for 29 days and drops to $695,000 on repayment day, you’ve paid interest on the higher balance almost the entire month.

If income reduces that balance early in the month — even temporarily — the interest calculation improves.

This is why average daily balance matters more than repayment timing alone.

When income hits the loan immediately, your money begins working against interest straight away.

Over 5, 10, 15 years, the compounding difference can be significant.

⸻

Is This Better Than an Offset?

The honest answer?

It depends on the client.

For disciplined savers who rarely dip into funds, an offset can perform similarly from a mathematical standpoint.

But for households that:

• Struggle with spending creep,

• Want stronger guardrails,

• Prefer visible progress,

• Need behavioural accountability,

This structure often produces superior outcomes — not because of rate advantage, but because of behavioural alignment.

It reduces temptation.

It builds momentum.

It keeps goals front of mind.

⸻

This Is Not About Financial Extremism

I am not advocating:

• Eliminating enjoyment.

• Living rigidly.

• Cancelling every subscription.

• Avoiding holidays.

This is about intentional structure.

It’s about ensuring:

• Income has a job.

• Debt reduction is automatic.

• Progress is visible.

• Spending is conscious.

Financial progress does not require suffering.

It requires systems.

⸻

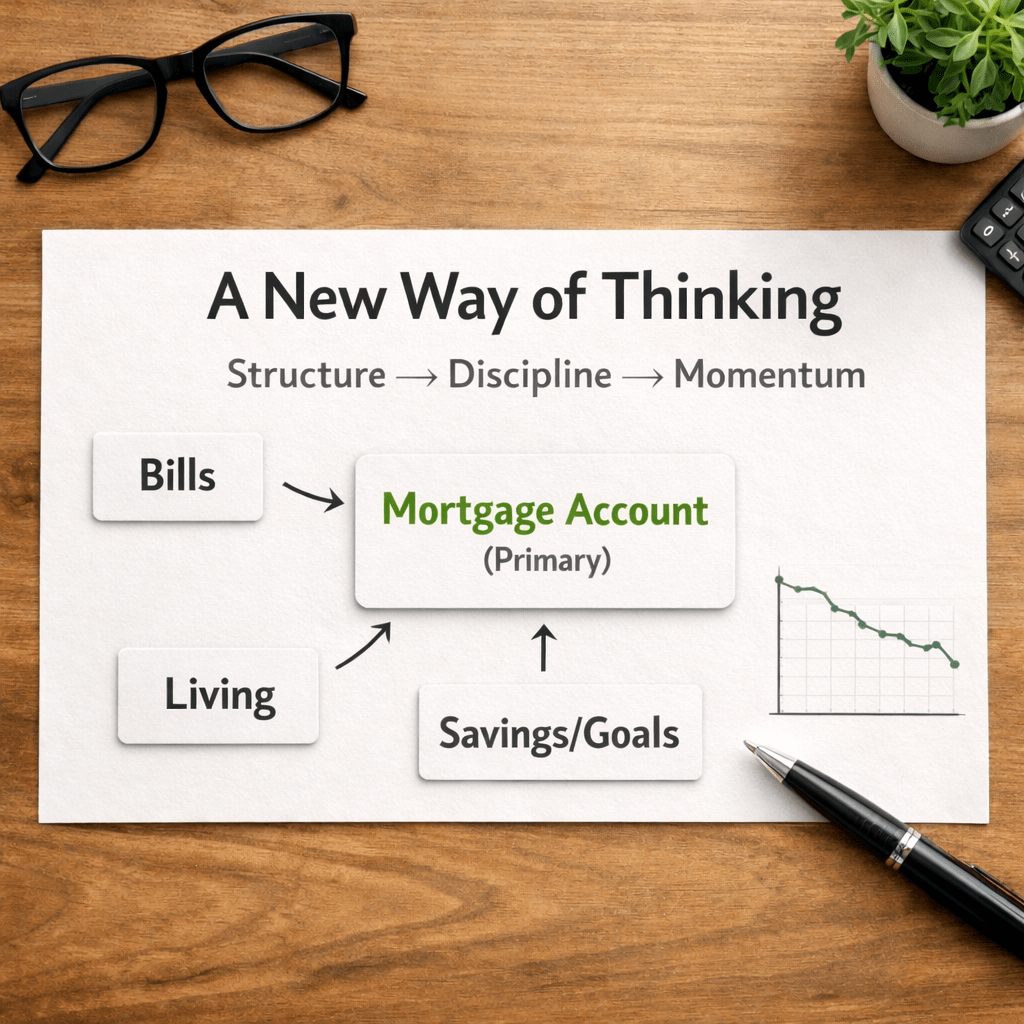

A New Way of Thinking. A Newstart to Finance.

Most households don’t need more income.

They need better flow.

When your mortgage becomes your primary financial account:

• Every pay cycle reduces debt.

• Every redraw becomes intentional.

• Every surplus dollar accelerates progress.

• Every month builds visible momentum.

For many clients, this structure creates something powerful:

Control.

Confidence.

Clarity.

It’s not just about paying off your home faster.

It’s about resetting how you think about money entirely.

A new way of thinking.

A Newstart to finance.

⸻

If you’d like to explore whether this structure suits your situation — and whether it complements or outperforms an offset in your case — I’m happy to walk through the numbers with you.

Because the best mortgage strategy is never just about rate.

It’s about structure, discipline, and execution over time.

Leave a comment